PRIVATE EQUITY IN ENERGY

The New Power Play: Private Capital Surge

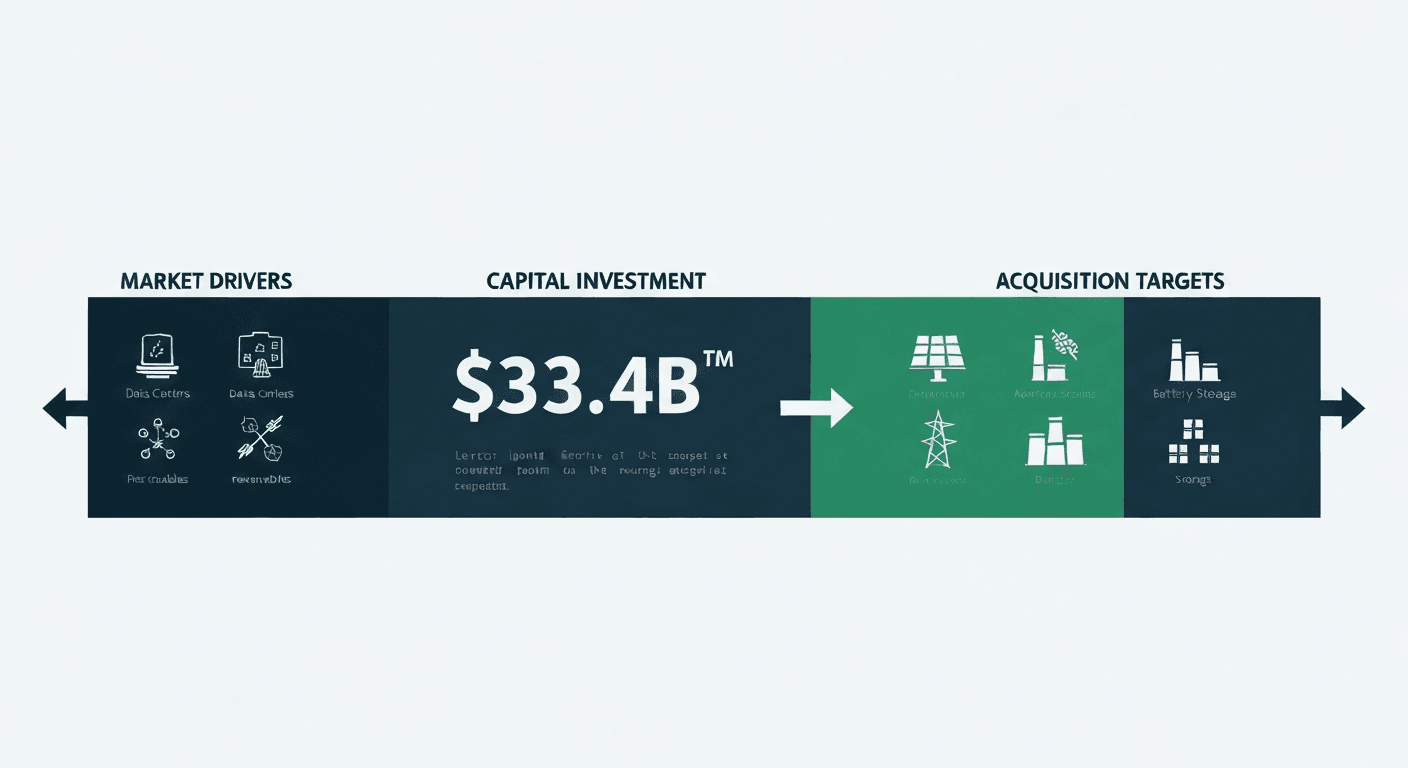

MARKET DRIVERS

- AI & Data Center Boom

- Energy Transition Capital Needs

- Grid Modernization Urgency

- Favorable Asset Valuations

Private Equity & Infrastructure Funds

ACQUISITION TARGETS

- Public Utilities (AES)

- Late-Stage Renewables

- Grid-Scale BESS

- Firm Capacity Portfolios

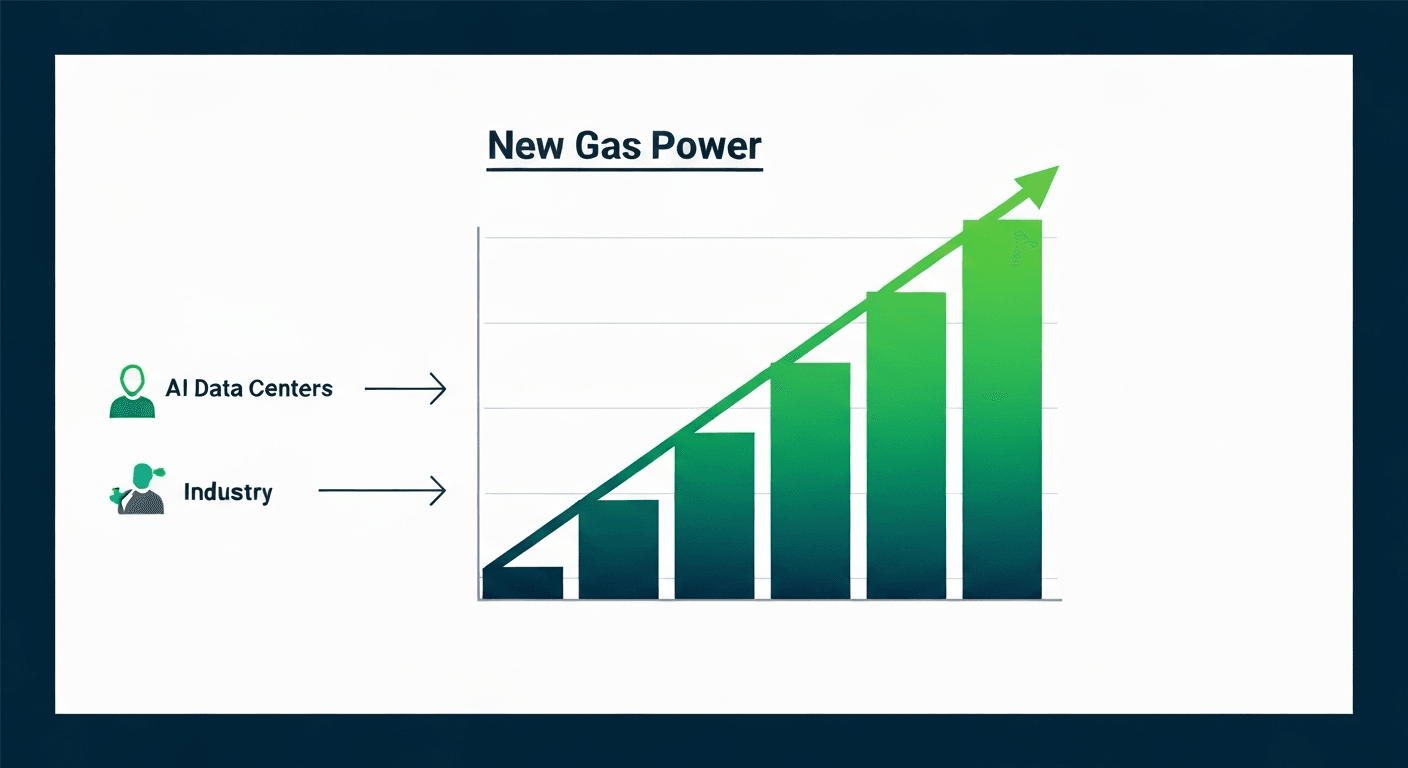

A landmark transaction this week signals a significant acceleration in the structural transformation of the U.S. power sector, driven by a torrent of private capital. A consortium led by Global Infrastructure Partners (GIP) and EQT announced a definitive agreement to acquire The AES Corporation in a massive $33.4 billion deal, taking one of the nation’s major publicly traded power producers private. This is not an isolated event but rather the most prominent example of a powerful emerging trend: the large-scale acquisition of energy infrastructure by private equity and specialized funds. These entities are positioning themselves to finance the monumental capital requirements of the energy transition and the explosive growth in electricity demand, a trend underscored by multiple reports this week on the power needs of AI and data centers.

The drivers behind this M&A surge are multifaceted. As highlighted by a new report from Mercom, declining valuations for solar and battery storage projects are creating a buyer’s market for sophisticated investors. In a higher interest rate environment, developers are finding it more challenging to finance projects, making them more amenable to acquisition. Private funds, with deep pockets and long-term investment horizons, are stepping in to acquire these de-risked, late-stage assets. They are specifically targeting portfolios that can provide the firm, reliable capacity—often solar-plus-storage—desperately needed to support a grid strained by data centers, as seen in states like Virginia, which is being called ‘ground zero’ for the demand surge.

The implications for the industry, including developers of Central Plants, CHP systems, and BESS, are profound. The influx of private capital can significantly accelerate the deployment of new technologies and grid modernization efforts. However, it also marks a fundamental shift in ownership and strategy, moving critical infrastructure from the purview of public markets to private hands. This transition will alter the competitive landscape, influence project development strategies, and likely lead to further consolidation. As institutional investors like BlackRock also make major plays, the industry must adapt to a new era where financial engineering and large-scale portfolio strategy are just as critical as technological innovation. Understanding the motivations and return criteria of these new capital allocators will be essential for success in the years ahead.

This Week’s Top 5 Energy News Items

- GIP and EQT-led consortium agree to acquire AES for $33.4bn

- Declining solar, storage valuations drive increased M&A: Mercom

- 600+ GWh of US energy storage expected by 2030: Benchmark/SEIA

- Politicians wake up to the data center dilemma

- Virginia targets surplus interconnection capacity in first-of-its-kind legislation

For more in-depth technoeconomic analysis of your energy projects, explore the capabilities of our CogenS platform.

Further Reading:

International Energy Agency – World Energy Investment Report

S&P Global Market Intelligence – Power and Utility M&A Analysis