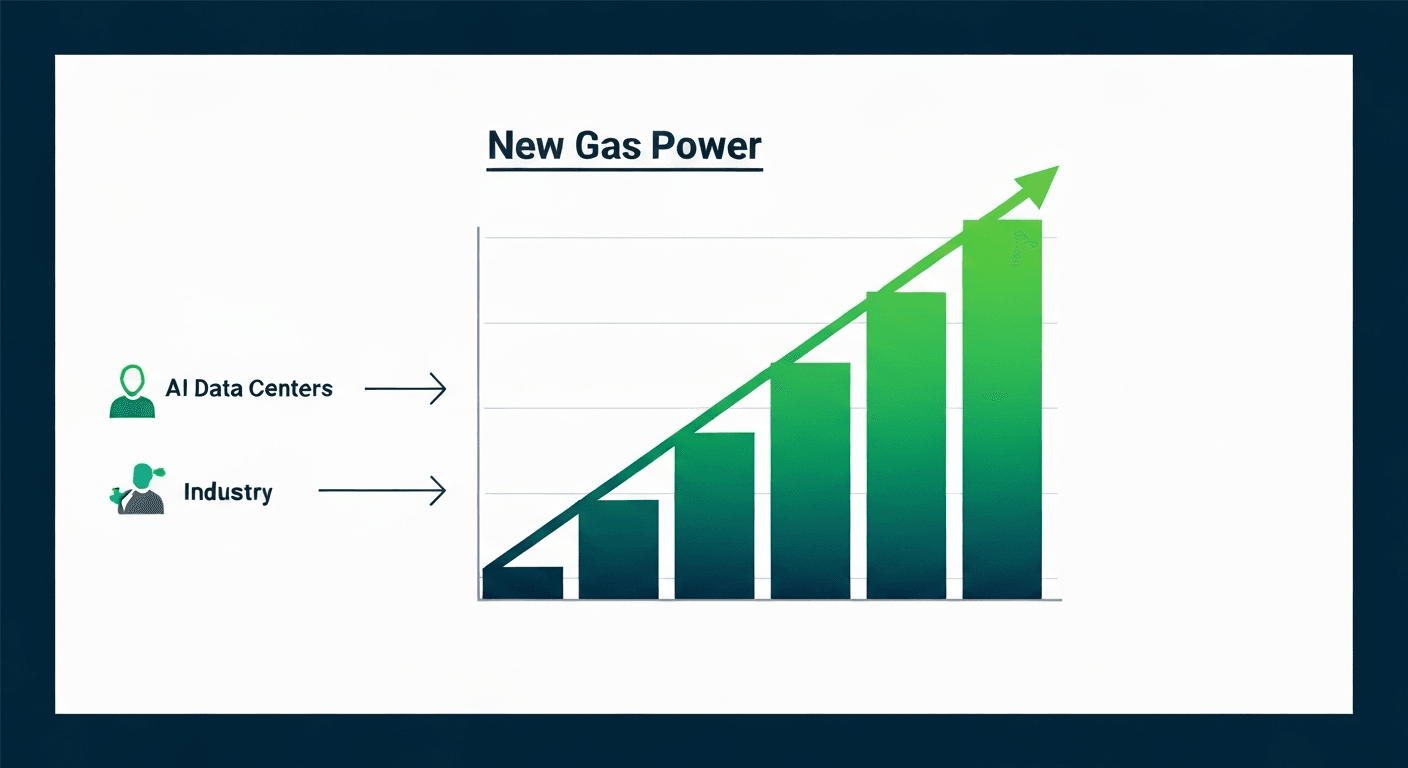

The New Gas Generation Rush: Firm Capacity to Meet Unprecedented Demand

9.5 GW

Texas & Pennsylvania

9.2 GW

Ohio

9.0 GW

US Portfolio by 2031

Major players announced nearly 28 GW of new natural gas projects this week, a direct response to soaring electricity demand forecasts driven by AI and data centers.

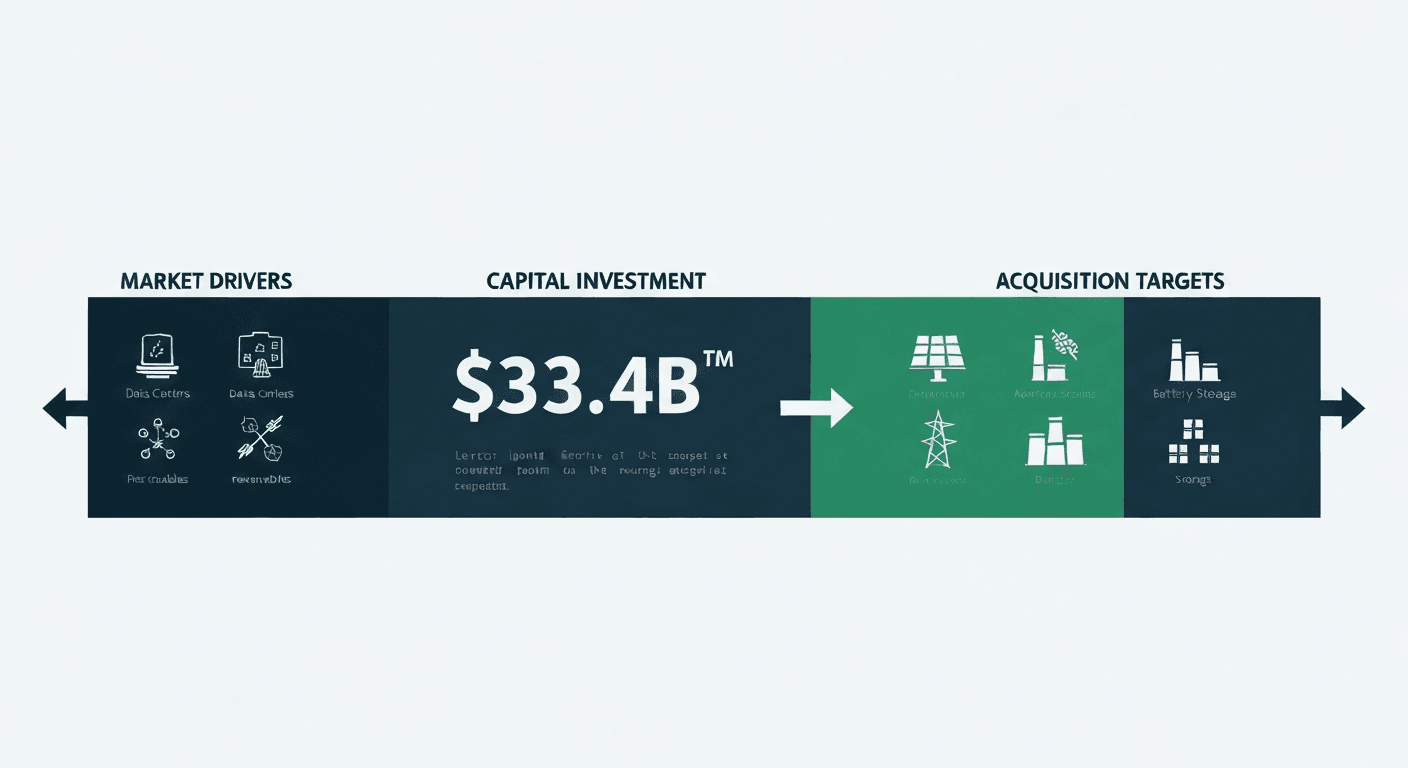

This week, the energy landscape was jolted by a series of monumental investment announcements signaling a powerful resurgence in natural gas-fired generation. In a stark reminder of the challenges posed by skyrocketing electricity demand, major energy developers unveiled plans for nearly 28 GW of new gas capacity in the U.S. These moves represent a pragmatic, if contentious, response to the urgent need for dispatchable, firm power to support a grid strained by the explosive growth of data centers, AI, and industrial electrification. The scale of these commitments suggests that while the long-term transition to renewables continues, the medium-term will heavily rely on gas to ensure reliability and meet load growth that is outpacing the deployment of clean energy and storage.

Leading the charge, NextEra Energy announced plans to develop a staggering 9.5 GW of gas generation in Texas and Pennsylvania. This was accompanied by news of a U.S.-Japan investment framework materializing into a 9.2 GW project in Ohio and up to another 10 GW from NextEra. Compounding this trend, European energy giant RWE declared its entry into the U.S. gas market with a 9 GW project pipeline slated for completion by 2031. These are not speculative ventures; they are direct, market-driven reactions to concrete demand signals. An EIA analysis this week explicitly stated that faster-than-expected growth in data center power demand could lead to a rise in fossil fuel generation, and these announcements are the first definitive materialization of that forecast.

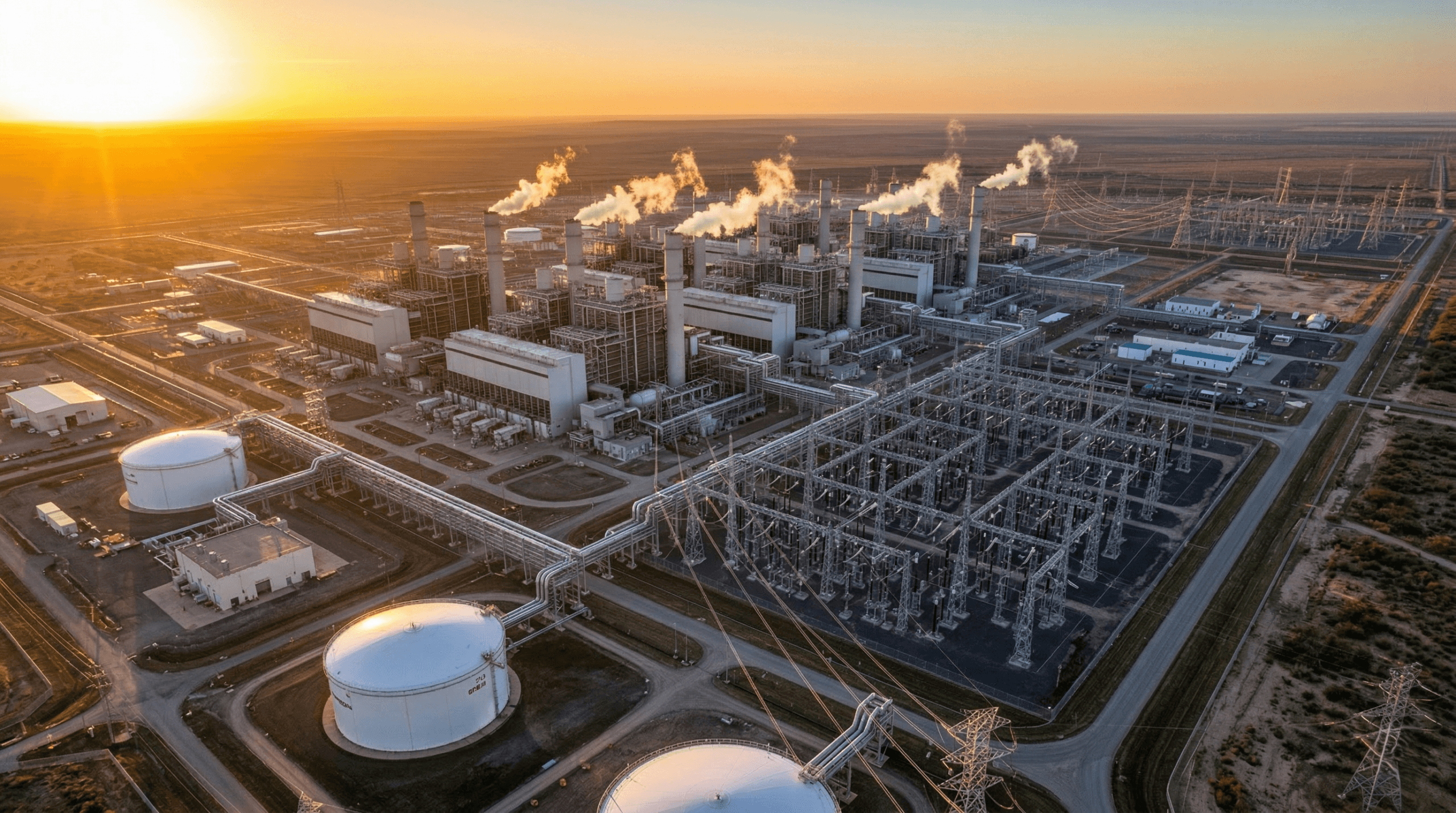

From a technoeconomic standpoint, the rationale is clear. While BESS deployment is accelerating and VPP legislation is emerging in states like Michigan and New York, the sheer gigawatt-scale and 24/7 reliability required by hyperscale data centers necessitate a level of firm capacity that current storage and renewable combinations struggle to guarantee, particularly given interconnection queue backlogs for clean resources. Gas turbines offer a mature technology with a shorter development timeline compared to nuclear and provide the operational flexibility needed to balance intermittent renewables. This trend also reflects deep-seated concerns about grid stability, particularly in markets like PJM, where recent crises have put a premium on reliable capacity. The on-site, 2 GW natural gas power solution for a West Virginia data center campus highlights a related trend of large loads bypassing the grid altogether to secure dedicated power.

This pivot back to gas, however, creates significant tension with long-term decarbonization goals. While some projects may be ‘hydrogen-ready’, they lock in fossil fuel infrastructure for decades. It underscores a critical juncture for the industry: how to reconcile the immediate, tangible needs for power and grid reliability with the strategic, essential imperative of the clean energy transition. This week’s developments firmly indicate that for the next decade, the answer will likely involve a significant and growing fleet of natural gas power projects operating alongside expanding renewable and storage assets.

This Week’s Top 5 Energy News Items

- NextEra to develop 9.5 GW of gas in Texas, Pennsylvania

- RWE announces first U.S. gas generation projects with 9 GW in the pipeline

- Fossil generation could rise with faster-than-expected growth in data center power demand

- Michigan, New York lawmakers consider virtual power plant bills

- Suddenly, the US manufactures a ton of grid batteries

For customized technoeconomic analysis of your energy projects, explore our CogenS software platform.

For further reading on energy trends, visit the U.S. Energy Information Administration and the International Energy Agency.